Strengthen Your Financial Health - One Step at a Time

Financial health looks different for everyone. No matter your goals, it starts with knowing where you stand - and having a clear view of your finances in one place helps you move forward with purpose. Every financial journey begins with small, manageable steps, and the right habits can help you build confidence along the way.

Simple Steps to Start Your Financial Health Journey

- Build a realistic budget. A workable budget starts with understanding both sides of your money: your income and your expenses. With a holistic view of all your finances in one place, you can stay aligned with your financial goals.

- Track your spending habits. Many of us spend more on non-essentials than we realize, like eating out, streaming services, and coffee runs. Understanding your spending patterns can help you stay intentional – even on days convenience wins.

- Build an emergency fund. Saving isn’t always easy – but an emergency fund can make unexpected moments easier to manage. Start small and stay consistent. Even modest contributions can make a meaningful difference over time.

- Plan for the future. When your day-to-day finances feel manageable, you can focus on bigger goals – like buying a car or house, traveling, or retirement. Mid American Credit Union supports you with the tools you need to be successful.

- Take it one step at a time. If managing your finances feels intimidating – you’re not alone. Financial health isn’t about perfection – it’s about progress and building confidence through steady habits.

We're Here to Help.

Financial health is a journey, but you don’t have to navigate it on your own. With the help of Mid American Credit Union, you can organize your finances, track your progress, and build a healthier, more secure future.

Meet Our Team.

.png)

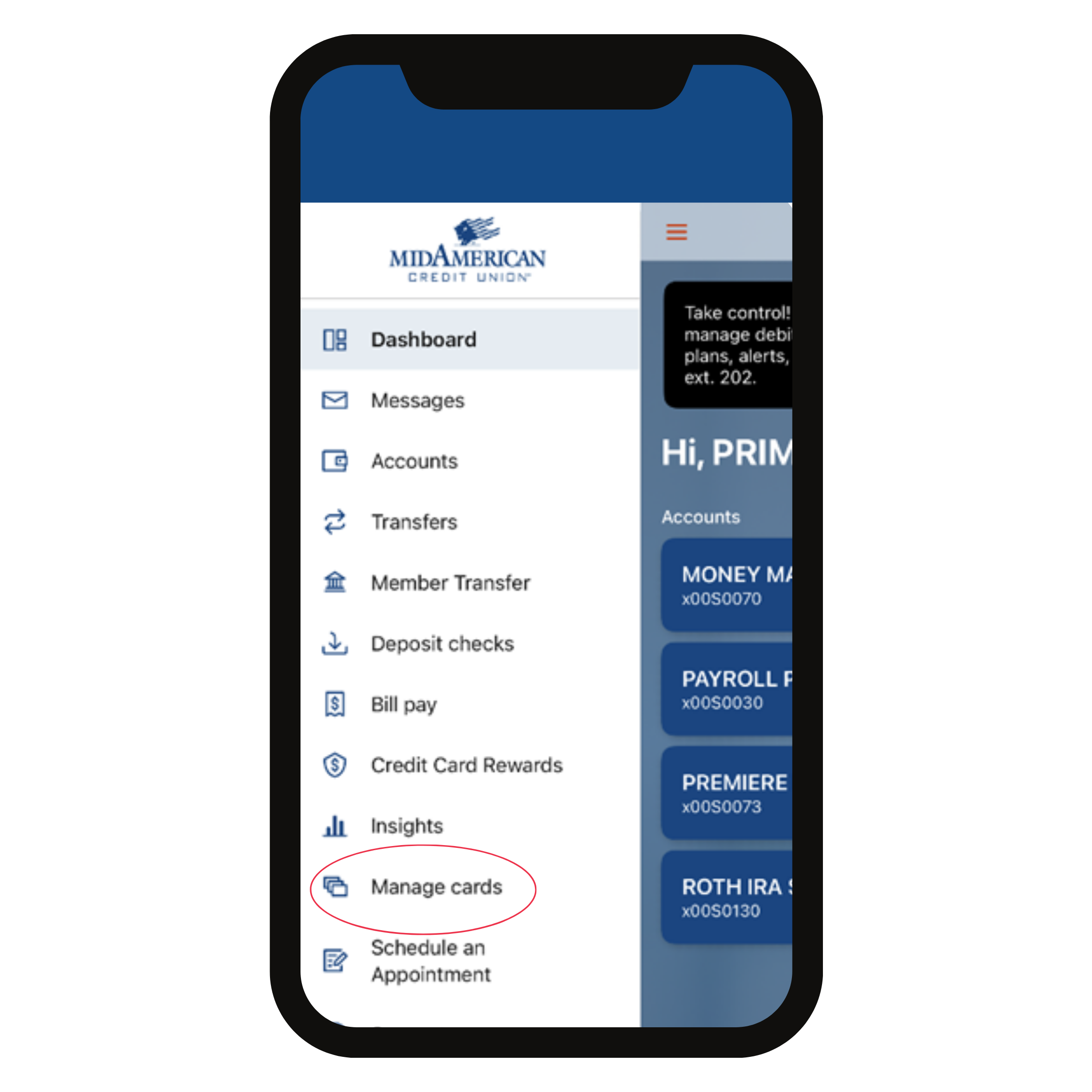

Use the Mid American Credit Union app to take control of your debit and credit cards.

HOW FAMILIES BUILD TRUE WEATH - ONE HABIT AT A TIME

HOW FAMILIES BUILD TRUE WEATH - ONE HABIT AT A TIMEThis short read helps parents teach kids the difference between active and passive income - with simple examples, hands-on ideas, and kid-friendly ways to build strong earning and saving habits early.

Read the article HERE

HOW TO TEACH KIDS ACCOUNTABILITY

This article helps parents teach kids how everyday choices, including spending, lead to real outcomes and learning moments.

Read the article HERE

12 BEST BOOKS TO TEACH YOUNG CHILDREN ABOUT MONEY

Are you looking for some of the best books to teach young children about money? We and our kids have done the leg work for you! We’ve reviewed books that teach the basics of money management all the way through investing for the future.

Read the article HERE

SNEAKY SHRINKFLATION

Have you ever opened a bag of chips and thought, Wait… didn’t there used to be more in here? You’re not imagining things. Many snacks really have gotten smaller—even though the price stayed the same.

This has a name: shrinkflation.

Read the full article HERE

HOW MUCH SHOULD YOU REALLY SPEND ON KIDS' ACTIVITIES? A FINANCIAL GUIDE FOR PARENTS.

HOW MUCH SHOULD YOU REALLY SPEND ON KIDS' ACTIVITIES? A FINANCIAL GUIDE FOR PARENTS. From soccer leagues to summer camps, kids’ activities can enrich your child’s life—but they can also drain your wallet. This financial guide helps parents navigate the true cost of extracurriculars, offering tips on budgeting, evaluating value, and making smart, values-driven decisions.

Read the full article HERE

INFLUENCERS: TRUE OR FALSE?

We all know we shouldn’t believe everything we hear… but sometimes we forget that applies to social media too. Not everything you see online is real. In fact, a lot of it is carefully staged to look real.

Some influencers are being called out for faking their wealth online.

Read the full article HERE

Take Action

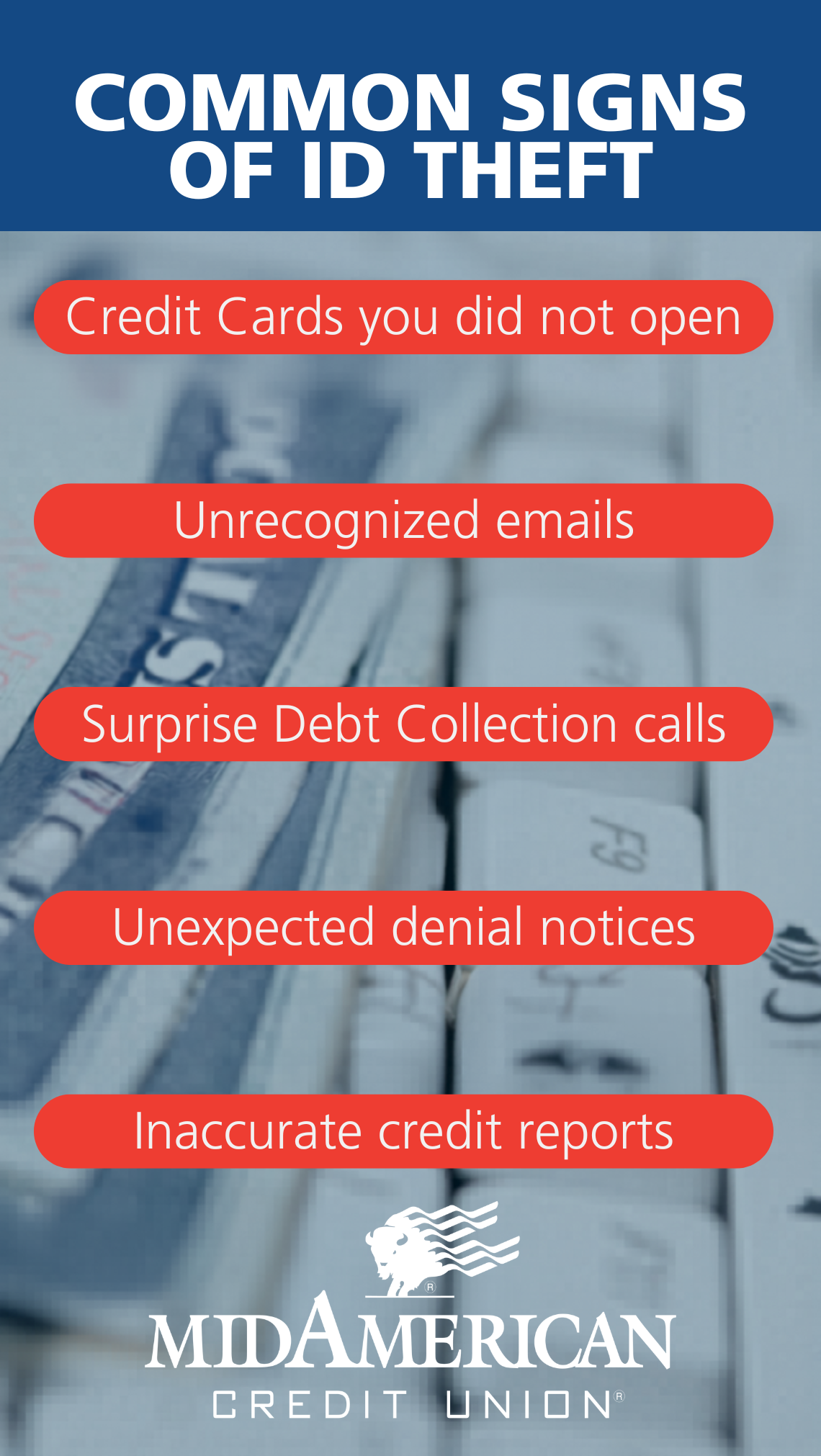

If you've been a victim of identity theft, here are ways you can take action:

- Report the identity theft to the Federal Trade Commission online at identitytheft.gov or call 877-438-4338.

- Contact the three major credit reporting agencies — Equifax, Experian and TransUnion — to put free fraud alerts and credit freezes on your accounts. With a fraud alert, creditors must verify your identity before opening a new account. With a credit freeze, you can still use your accounts, but no new accounts can be opened in your name. To lift the freeze temporarily (if you’re applying for a loan, new job or other reasons), you need to contact each credit bureau and follow the instructions to verify your identity.

- Notify your financial institutions, credit card issuers and any other entity where you have accounts that you’ve been a victim of fraud.

If you have a checking account with Mid American Credit Union, you have extra protection through our free victim resolution service. - Monitor your credit reports. You’re entitled to one free report every year from each of the three credit reporting agencies. Annualcreditreport.com is the only federally authorized source for those free reports. If you make a request to a different agency every four months, you can get year-round monitoring.

Ways to Protect Yourself

To help reduce your risk of identity theft, here are some things you can do:

- Don’t share your bank account numbers, Social Security number or other types of account and personal information to someone who calls, texts or emails you. Your credit union or bank already has that information, so they wouldn’t call, text or email you for that. Avoid responding to emails that ask you to click on links to verify information. Don’t give in to callers who make high-pressure demands for that information.

- Store documents securely at home. Don’t carry your Social Security card in your wallet; if you need it for a specific reason, put it back in a secure place after you’ve used it.

- Limit which credit cards you use for online purchases. It’s easier to track activity on one or two cards.

- Check your banking and credit card statements regularly to monitor activity. If you get statements by regular mail, note when they are delivered; if they don’t arrive on time, follow up with the company. Choose paperless or e-statements to reduce the risk of paper statements being intercepted.

Many financial and credit institutions have apps where you can get quick, real-time access. Some even allow you to put restrictions on using your debit or credit cards, like Mid American’s Card Manager app. - Shred receipts, unsolicited applications for cards or loans, bank or medical statements or other such documents.

- Use unique, strong passwords for each online account and a two-factor authentication process for online accounts. To track passwords, use an online password manager or app. With two-factor authentication, you’ll need to provide a second type of verification, like a code sent to your email or phone.

What do you want to learn about today?

Budgeting & Saving

Creating a Budget that Works

- A budget is one of the backbones of a healthy financial life. Having one sets you up for financial success.

- A budget should:

- provide freedom.

- shows me how much I can spend on the fun things in life.

- helps me reach my long-term and short-term savings goals.

- gives me direction to keep my financial life in order so that I can do the things I want to do.

- A budget should:

Building an Emergency Fund

- According to a recent report, 56 percent of American adults have dealt with a “surprise expense” within the last year. The average cost of that expense was a whopping $5,500. What does that mean? It means a healthy emergency fund is necessary.

Setting and Reaching Savings Goals

- Short Term Goal

- Set a Budget. Make sure you have a solid budget in place. It’s hard to obtain any financial stability if you don’t know how much money is coming and how much is going. If you have a budget already, make it a habit to review it every six months.

- Pay Down Debt. Create a plan to pay down your debts. While we recommend the avalanche method (paying down the higher-interest debt first), use whatever works best for you.

- Create an Emergency Fund. Set up a savings account for emergency expenses. You want to save at least six months’ worth of fixed expenses.

Tips for Cutting Everyday Expenses

- Cancel Subscriptions

- Go through your subscriptions and cancel any that you haven’t used recently.

- Cut back

- Once you have canceled subscriptions, comb through your budget for areas where you can reduce additional spending. Example: Entertainment, Eating out and Travel

- Make it automatic

- One easy way to increase your savings is to set up an automatic deposit into your accounts. Each paycheck, make sure a certain amount goes into your savings before you even have a chance to spend it. Out of sight, out of mind.

Credit & Debt Management

Understanding Your Credit Score

- Your credit score is a three-digit number that shows how well you manage borrowed money. It’s based on things like your payment history, how much debt you have, and how long you’ve had credit. Scores usually range from 300 to 850 the higher, the better. A good credit score can help you get approved for loans, lower interest rates, and even better job opportunities. By paying your bills on time, keeping your credit card balances low, and checking your credit report regularly, you can build and maintain a healthy credit score.

Smart Credit Card Use

- Using a credit card wisely can help you build good credit and avoid debt. Always try to pay your balance in full each month to avoid interest charges. Keep your spending within your budget, and use only a small portion of your credit limit. Making payments on time and keeping track of your purchases are key to staying in control of your credit.

Debt Consolidation Options

-

Debt consolidation is a way to combine multiple debts into one monthly payment, often with a lower interest rate. This can make managing your bills easier and help you pay off debt faster. Common options include personal loans, balance transfer credit cards, or working with a credit union like Mid American to find the best solution for your situation.

Student Loan Repayment Strategies

- Paying off student loans can feel overwhelming, but with the right plan, it’s manageable. Start by knowing your loan types, due dates, and interest rates. Consider setting up automatic payments to avoid missed due dates, and pay a little extra when you can to reduce interest over time. If you’re struggling, look into income-driven repayment plans, deferment, or refinancing options. Mid American Credit Union can help you explore strategies that fit your budget and long-term goals.

Avoiding Debt Traps

- Debt traps happen when borrowing becomes hard to manage, often leading to more debt over time. To avoid them, borrow only what you truly need and understand the terms before taking out any loan or credit card. Make a budget and stick to it, keeping track of spending and payments. Avoid relying on high-interest options like payday loans or only making minimum payments.

Home & Auto Financing

Buying vs. Renting a Home: Buying a home offers loan-term financial and personal benefits.

- Building equity

- Potential tax advantages

- Increased flexibility

Understanding Mortgage Basics

- Main types of mortgage loans: Conventional, FHA, VA and USDA Loans

- Types of interest rates on a mortgage: Adjustable-rate or Fixed-rate mortgage

- Most common mortgage loan terms: 10,15, and 30 years

- For any questions, contact our mortgage department:

Using Home Equity Wisely

- You can use the equity in your home to take out a loan that uses your property as collateral. You could use the funds to provide additional monthly funds for living expenses, pay for repairs to your home, home improvements, or debt consolidation. If you fail to make payments or meet other loan requirements, you could be at risk of losing your home through foreclosure.

- Set a Budget

- Check your credit score

- Get Pre-Approved for a loan:

- Shop around

- Negotiate the price

- Review contract carefully

Investing & Retirement

Investing 101

- Investing for Retirement. If you’re saving for retirement, one rule of thumb is to save between 10 and 15 percent of your yearly income.

- Workplace Retirement Plan. If you have a 401(k) at work, make sure you are maxing out your contributions. That’s especially true if you have an employee match (which can count toward your 15 percent). That’s free money and you don’t want to miss out.

- Other Investment Goals. If you’re saving for something like a house, consider how much you’ll need and work out a budget that will help you get to that goal in the timeframe you’ve set for yourself.

How Compound Interest Works

- Compound interest is when you earn interest on the money you’ve saved and on the interest you earn along the way.

Planning for Retirement

- If you haven’t started saving for retirement, do so immediately. Also, save as much as you can, while you can.

- Here are some ways to help you save money, starting today:

- Go through your budget and trim excess spending.

- Funnel that money into your retirement savings accounts and investments.

- If you have an employer match on your 401(k), make sure you contribute enough to get the match, if not more.

- If you don’t have a 401(k), open an IRA as a retirement savings vehicle.

- Aim to save between 10 to 15 percent of your pretax income. If you can go higher than that, all the better. The main point is to start saving now and save as much as you can.

Risk vs. Reward

- Starting with a simple investment, like an S&P 500 ETF, can help you gain confidence and experience.

Why an Emergency Fund Matters

Unexpected expenses happen. An emergency fund helps you stay in control when they do! Here’s what to know:

Unexpected expenses happen. An emergency fund helps you stay in control when they do! Here’s what to know:

- How Much Should You Save? A common goal is 3 to 6 months of essential living expenses. If that feels overwhelming, start smaller, such as a month of expenses or a set percentage of each paycheck.

- What Counts as an Emergency? True emergencies are unexpected and necessary expenses like medical bills, urgent car repairs, job loss, or essential home repairs.

- What Doesn’t Count? Planned purchases, vacations, or non-essential spending should be saved for separately.

- How to Get Started: Set a realistic monthly savings goal and keep your emergency fund in a separate, easily accessible savings account. Better yet, set up automatic deposits for each pay period so your emergency savings can grow without you having to make a manual contribution each time.

Even small, consistent contributions can build a strong financial safety net over time!

Smart Ways to Use Your Tax Refund

Receiving a tax refund can feel like a financial boost. Having a plan for it can help you make the most of it!

Receiving a tax refund can feel like a financial boost. Having a plan for it can help you make the most of it!

Here are smart ways to use your refund:

- Build or Boost Your Emergency Fund: Strengthening your savings can help cover unexpected expenses.

- Pay Down High-Interest Debt: Applying your refund toward credit cards, personal loans, or other high-interest balances may reduce long-term interest costs.

- Catch Up on Bills: If you’re behind on payments, your refund can help bring accounts current.

- Save for a Goal: Consider setting aside funds for a future expense like a home purchase, education, or major purchase.

-

Invest in Yourself: Professional certifications, training, or skills development can pay off long term.

A thoughtful plan can turn a one-time refund into lasting financial progress!

Understanding Retirement Accounts

Saving for retirement doesn’t have to feel overwhelming. Understanding the different categories of retirement accounts is a great place to start!

Saving for retirement doesn’t have to feel overwhelming. Understanding the different categories of retirement accounts is a great place to start!- Employer-Sponsored Plans: Offered through your workplace and often funded through automatic paycheck contributions. Some employers may also offer matching contributions. Common examples include 401(k) plans, 403(b) plans, and pensions.

- Individual Retirement Accounts (IRAs): Personal retirement accounts you open independently. Traditional IRAs may allow tax-deductible contributions today, with taxes paid when withdrawals are made in retirement. Roth IRAs are funded with after-tax dollars, but qualified withdrawals during retirement are generally tax-free.

- Self-Employed Retirement Plans: Designed for individuals who work for themselves or run their own business. A common option is a Simplified Employee Pension (SEP) IRA, which allows higher contribution limits compared to many personal retirement accounts.

- Small Business Retirement Plans: Plans created for small businesses with employees. A SIMPLE IRA allows both employers and employees to contribute, helping workers build retirement savings through workplace participation.

The right option depends on factors like income, employment status, and long-term financial goals. Getting familiar with these account types can help you take the next step toward building long-term retirement savings!

What is the NCUA?

- Coverage Limit: Insures deposits up to $250,000 per member, per insured credit union, per ownership category.

- What’s Covered? Checking accounts, savings accounts, money market accounts, and CDs—your standard share deposit accounts.

- What’s NOT Covered? Investments like stocks, bonds, mutual funds, crypto assets, or life insurance policies.

- How to Confirm Coverage? Visit the NCUA website to verify your credit union is federally insured.

Since Mid American Credit Union is NCUA-insured, your deposits are protected with built-in federal coverage!

What Does the Equal Housing Lender Logo Mean?

![]() When you see “Equal Housing Lender”, it’s more than just a logo. It represents a commitment to fairness in housing.

When you see “Equal Housing Lender”, it’s more than just a logo. It represents a commitment to fairness in housing.

Here’s what that means:

- Fair Lending Laws: Banks and credit unions follow federal laws, including the Fair Housing Act, that prohibit discrimination in housing-related lending.

- Equal Opportunity for Applicants: Qualified borrowers cannot be denied or treated differently based on race, color, religion, national origin, sex, disability, or familial status.

- Consistent Lending Standards: All applicants are evaluated using the same criteria and lending guidelines.

The Equal Housing Lender designation reflects a commitment to fair access and equal opportunity in housing for every qualified applicant.